Understanding How FICO Scores Are Calculated

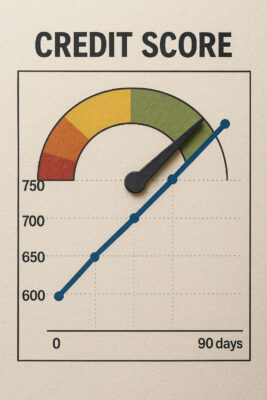

When it comes to borrowing, your FICO score is one of the most influential numbers in your financial life. Developed by the Fair Isaac Corporation, this credit score ranges from 300 to 850, with higher scores indicating lower lending risk. Generally, scores above 670 are considered “good,” while those below can make obtaining loans difficult or expensive.

When it comes to borrowing, your FICO score is one of the most influential numbers in your financial life. Developed by the Fair Isaac Corporation, this credit score ranges from 300 to 850, with higher scores indicating lower lending risk. Generally, scores above 670 are considered “good,” while those below can make obtaining loans difficult or expensive.

What many consumers don’t realize is that the FICO score is not a static measurement—it’s a calculated result of several weighted factors:

- 35% – Payment history: A record of on-time vs. late payments.

- 30% – Amounts owed: The ratio of current debt to available credit.

- 15% – Length of credit history: How long your accounts have been established.

- 10% – Credit mix: A variety of credit types, such as credit cards, auto loans, and mortgages.

- 10% – New credit inquiries: How many new accounts you’ve recently applied for.

This breakdown, while well-known, only scratches the surface of a much deeper algorithmic system.

Hidden Factors Behind Credit Modeling

For most consumers, the concept of a credit score begins and ends with a three-digit number. But what’s often missing from public understanding is just how complex and opaque credit modeling truly is. That’s no accident. The methodologies used to calculate a FICO score are protected intellectual property, deeply proprietary, and—perhaps most notably—not designed for public transparency.

While the standard explanation for a FICO score references the basic five components—payment history, amounts owed, length of credit history, credit mix, and new credit inquiries—the real formula is far more intricate.

Proprietary Algorithms and Behavioral Predictions

At its core, a FICO score is generated by predictive modeling software that incorporates not just raw financial data but also behavioral indicators and statistical correlations. Here are some of the hidden or lesser-known factors that can significantly influence your score:

- Trended Data: Instead of a simple snapshot of your credit utilization, newer models use “trended data,” which analyzes your credit usage patterns over time. Are you consistently paying down balances, or just making minimum payments? Are your credit limits gradually increasing or decreasing? These behavioral trends offer deeper insights into financial responsibility.

- Utilization Timing: Your reported balance can depend on when a creditor submits data to the bureaus, which may not align with your payment schedule. Even if you pay in full each month, a high balance reported mid-cycle can skew your utilization ratio and impact your score. This temporal mismatch is often overlooked by consumers.

Credit Score Version Variability

One of the most misunderstood elements in credit modeling is that there isn’t just one FICO score. In fact, there are dozens of score versions, each tailored to a specific lending context. For example:

One of the most misunderstood elements in credit modeling is that there isn’t just one FICO score. In fact, there are dozens of score versions, each tailored to a specific lending context. For example:

- FICO Score 8 is the most commonly used version by general lenders.

- FICO Score 9 places less emphasis on medical collections.

- FICO Auto Scores and FICO Bankcard Scores are fine-tuned for their respective lending environments.

- FICO Score XD incorporates alternative data like utility and telecom payments for consumers with limited credit history.

Each version assigns different weights to the same inputs, and lenders have discretion over which version they use. That means a consumer could appear highly creditworthy under one model, yet borderline risky under another.

This variability raises important legal considerations. Consumers are often unaware which version is being used to evaluate their application, and more importantly, they are not given full visibility into the precise metrics that drove a lender’s decision.

Why It Matters

In practice, this lack of transparency can affect everything from interest rates and loan approvals to employment background checks and insurance premiums. When a single number carries this much weight, consumers deserve clarity—yet the current system obscures the full picture.

As attorneys, we often see the fallout of this opacity when clients come to us confused about a denial, misinformed about what actually impacts their credit, or facing the repercussions of outdated or inaccurate reporting. With the rise of alternative data and fintech lending, these models will only grow more complex, further distancing consumers from the mechanics that govern their financial opportunities.

Why Alternative Credit Data Is Pressuring FICO

A significant shift is underway. As reported by PYMNTS.com, alternative data is emerging as a challenge to traditional credit modeling. Newer credit scoring models and fintech platforms are incorporating:

- Rent and utility payment history

- Bank account cash flow

- Subscription and telecom payments

- Income streams

This trend is partly driven by the need to assess “credit invisibles”—people with thin or no credit files. The result is growing pressure on traditional FICO scores to adapt or risk becoming less relevant.

The Legal Implications of Credit Scoring

For consumers, this system raises legal questions, especially around transparency and fairness. The Equal Credit Opportunity Act (ECOA) and the Fair Credit Reporting Act (FCRA) require that scoring models avoid discrimination and give consumers the right to dispute inaccurate information. However, with the increasing complexity of credit modeling and the rise of AI-driven underwriting, these safeguards may not go far enough.

From a legal perspective, the opacity of FICO’s algorithm presents a challenge. Consumers are rarely told which score version is used or how specific behaviors affected their score. This lack of transparency can result in unfair denials and inflated borrowing costs—particularly for vulnerable populations.

How Consumers Can Improve Credit Scores

Improving your credit score requires strategic action:

Improving your credit score requires strategic action:

- Always pay bills on time.

- Keep credit card balances below 30% of the limit.

- Avoid unnecessary new credit inquiries.

- Build a mix of revolving and installment credit.

- Regularly check your credit reports from Equifax, Experian, and TransUnion.

In light of the growing influence of alternative data, consumers might also consider using servicers that report rent or utility payments to credit bureaus. These service providers can supplement thin credit files and help consumers get fairer access to credit.

If you’re experiencing challenges related to credit scores—such as inaccurate reporting, loan denials, or confusion over score discrepancies—consulting with an attorney who understands the evolving credit landscape can make a significant difference. Legal insight ensures your rights are protected, especially as new credit modeling practices continue to reshape the financial system.

Disclosure: This article is intended for informational purposes only and should not be considered legal advice. Images included are used for illustrative and artistic purposes only and do not depict actual individuals, events, or specific locations.

____________________________________

Led by attorneys J. Andrew Meyer and Michael D. Finn with over 75 years of combined legal experience. The Finn Law Group is a national consumer protection firm that specializes in Timeshare Law. If you feel you need the services of a timeshare attorney, contact our law firm today at 855-FINN-LAW. Want to learn more on timeshare related issues? Follow us on X.