CFPB Moves to Define Consumer Risk

The Consumer Financial Protection Bureau (CFPB) announced a new proposal that could change how it supervises certain financial companies. The rule is designed to give a clear definition of what counts as a “risk to consumers” when people use financial products or services.

The Consumer Financial Protection Bureau (CFPB) announced a new proposal that could change how it supervises certain financial companies. The rule is designed to give a clear definition of what counts as a “risk to consumers” when people use financial products or services.

Right now, the Bureau has the legal power to watch over nonbank financial companies—businesses that offer loans or services but are not traditional banks. These include payday lenders, debt collectors, mortgage companies, and fintech firms. However, until recently, the CFPB rarely used this power. When it did, the Bureau decided what “risk” meant case by case, leaving companies unsure of where they stood.

The proposed rule would finally set a standard definition. According to the CFPB, conduct would be considered risky if it:

- Has a high chance of causing significant harm to consumers, and

- Is directly connected to a financial product or service.

Why the “Consumer Risk” Rule Matters

For Consumers

For Consumers

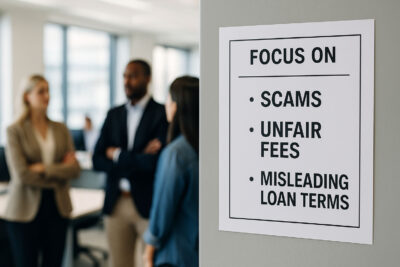

This change would mean stronger and clearer protection from harmful practices. Instead of the Bureau spreading its attention across minor issues, it would focus on the most serious problems—like scams, unfair fees, or misleading loan terms that could cost people money or damage their credit.

For Companies

Nonbank financial companies would also benefit because they would finally know the rules. A standard definition would create predictability and reduce the chances of sudden investigations. The Bureau even noted that fewer companies might be targeted once this clearer standard is in place.

For the CFPB

By focusing on serious, well-defined risks, the Bureau can use its resources more effectively. This allows it to target companies that cause real harm instead of chasing after smaller concerns.

Examples of Nonbank Lenders and Companies Affected

The proposed rule mainly applies to nonbank financial companies, which can cover a wide range of businesses. Some of these are known for high-risk behavior, especially if they take advantage of consumers. Examples include:

The proposed rule mainly applies to nonbank financial companies, which can cover a wide range of businesses. Some of these are known for high-risk behavior, especially if they take advantage of consumers. Examples include:

- Payday lenders – Offer short-term, high-interest loans that can trap borrowers in cycles of debt.

- Auto-title lenders – Provide loans using a car title as collateral, often with extremely high fees and repossession risks.

- Mortgage companies and servicers – Some have been known to mishandle payments, charge unfair fees, or use confusing paperwork.

- Student loan servicers – Risky practices include misapplying payments, failing to inform borrowers of repayment options, or adding unnecessary fees.

- Debt collectors – Can cause harm through harassment, false threats, or collecting debts not actually owed.

- Fintech companies (apps and online lenders) – While innovative, some have little oversight and may engage in risky practices like unclear terms, hidden fees, or misuse of consumer data.

- Buy Now, Pay Later (BNPL) companies – These are growing rapidly but may pose risks if consumers are not told about late fees, interest, or how multiple loans can quickly add up.

- Timeshare lenders and resort financing companies – Often tie consumers into long-term, high-cost obligations with confusing contracts, hidden fees, and limited exit options, which can leave families financially stuck.

What to Watch For

As this rule moves forward, here are some key things to pay attention to:

- Public Comments – Consumer groups and industry representatives will likely submit strong opinions that could shape the final rule.

- Final Rule Language – Watch whether the Bureau keeps the narrower focus on “serious, non-speculative risks” or broadens its reach again.

- Consumer Protection Shifts – If adopted, the Bureau may redirect its energy toward the worst offenders, meaning less action against borderline cases but tougher action against clear harm.

- Industry Pushback – Expect resistance from some nonbank lenders who may argue that the rule goes too far, even though the CFPB says it will likely reduce the number of companies being targeted.

Final Thoughts on CFPB Rulemaking

The CFPB’s proposal is more than just a technical rule—it represents an important step toward balancing the needs of consumers and the financial companies. For everyday people, the rule could mean fewer surprises, fewer hidden traps, and stronger protection against unfair practices that can take a heavy toll on families’ finances. Whether it’s a payday loan with crushing interest, a student loan servicer that mishandles payments, or a timeshare contract that feels impossible to escape, the risks are real and deeply personal.

For companies, the rule offers much-needed clarity. Instead of facing uncertainty about when and how the Bureau might step in, businesses will have a clearer understanding of what behaviors cross the line. That predictability can help responsible lenders operate with confidence while ensuring that those who engage in risky or harmful practices are held accountable.

At its heart, this proposal reflects the CFPB’s effort to focus its energy where it matters most—on serious, meaningful risks that cause real harm. And for consumers navigating an already complicated financial landscape, that attention can make all the difference.

Disclosure: This article is intended for informational purposes only and should not be considered legal advice. Images included are used for illustrative and artistic purposes only and do not depict actual individuals, events, or specific locations.

At Finn Law Group, we have long advocated for consumer protection through both federal and state agencies. Timeshare ownership can be overwhelming, with complex contracts, aggressive sales tactics, and industry practices that often leave consumers feeling misled or powerless. Our role is to stand up for your rights, explain what legal changes may mean for you, and bring clarity to a system that too often feels stacked against timeshare owners.

Led by timeshare attorneys J. Andrew Meyer and Michael D. Finn, who bring over 75 years of combined legal experience, Finn Law Group is a national consumer protection firm dedicated exclusively to Timeshare Law. If you believe you need the services of an experienced timeshare attorney, contact us today at 855-FINN-LAW. Want to stay informed on timeshare-related issues? Follow us on X (formerly Twitter) for updates and insights.